SEC Completes Inflation Adjustment Under Titles I And III Of The Jobs Act; Adopts Technical Amendments

On March 31, 2017, the SEC adopted several technical amendments to rules and forms under both the Securities Act of 1933 (“Securities Act”) and Securities Exchange Act of 1934 (“Exchange Act”) to conform with Title I of the JOBS Act. On the same day, the SEC made inflationary adjustments to provisions under Title I and Title III of the JOBS Act by amending the definition of the term “emerging growth company” and the dollar amounts in Regulation Crowdfunding.

Title I of the JOBS Act, initially enacted on April 5, 2012, created a new category of issuer called an “emerging growth company” (“EGC”). The primary benefits to an EGC include scaled-down disclosure requirements both in an IPO and periodic reporting, confidential filings of registration statements, certain test-the-waters rights in IPO’s, and an ease on analyst communications and reports during the EGC IPO process. For a summary of the scaled disclosure available to an EGC as well as the differences in disclosure requirements between an EGC and a smaller reporting company, see HERE.

As a reminder, the definition of an EGC as enacted on April 5, 2012 (i.e., not including the new inflationary adjustment discussed in this blog) is a company with total annual gross revenues of less than $1 billion during its most recently completed fiscal year that first sells equity in a registered offering after December 8, 2011. An EGC loses its EGC status on the earlier of (i) the last day of the fiscal year in which it exceeds $1 billion in revenues; (ii) the last day of the fiscal year following the fifth year after its IPO (for example, if the issuer has a December 31 fiscal year-end and sells equity securities pursuant to an effective registration statement on May 2, 2016, it will cease to be an EGC on December 31, 2021); (iii) the date on which it has issued more than $1 billion in non-convertible debt during the prior three-year period; or (iv) the date it becomes a large accelerated filer (i.e., its non-affiliated public float is valued at $700 million or more). EGC status is not available to asset-backed securities issuers (“ABS”) reporting under Regulation AB or investment companies registered under the Investment Company Act of 1940, as amended. However, business development companies (BDC’s) do qualify.

The provisions of Title I of the JOBS Act were self-executing and automatically became effective on April 5, 2012. Although the SEC has passed several rules and made numerous form amendments to conform to the JOBS Act provisions, several of the rules and forms under the Securities Act, Exchange Act, periodic and current reports forms, Regulation S-K and Regulation S-X did not reflect the JOBS Act provisions.

The statutory definition of an EGC, as reflected in Securities Act Section 2(a)(10) and Exchange Act Section 3(a)(80), require the SEC to make an adjustment to index to inflation the annual gross revenue amount used to determine an EGC, every five years.

Likewise, Title III of the JOBS Act, which set the statutory groundwork for Regulation Crowdfunding, requires an inflationary adjustment to the dollar figures in Regulation Crowdfunding every five years. On March 31, 2017, the SEC did so for the first time.

Inflation Adjustments

Definition of “Emerging Growth Company”

The JOBS Act amended Section 2(a)(19) of the Securities Act and Section 3(a)(80) of the Exchange Act to define an “emerging growth company” to mean a company with total annual gross revenues of less than $1 billion, as adjusted for inflation every 5 years, during its most recently completed fiscal year that first sells equity in a registered offering after December 8, 2011.

The SEC is now making its first inflationary increase to the definition. The inflation increase is $70,000. Accordingly, an EGC is now defined as a company with total gross revenues of less than $1,070,000,000.

Regulation Crowdfunding Amendments

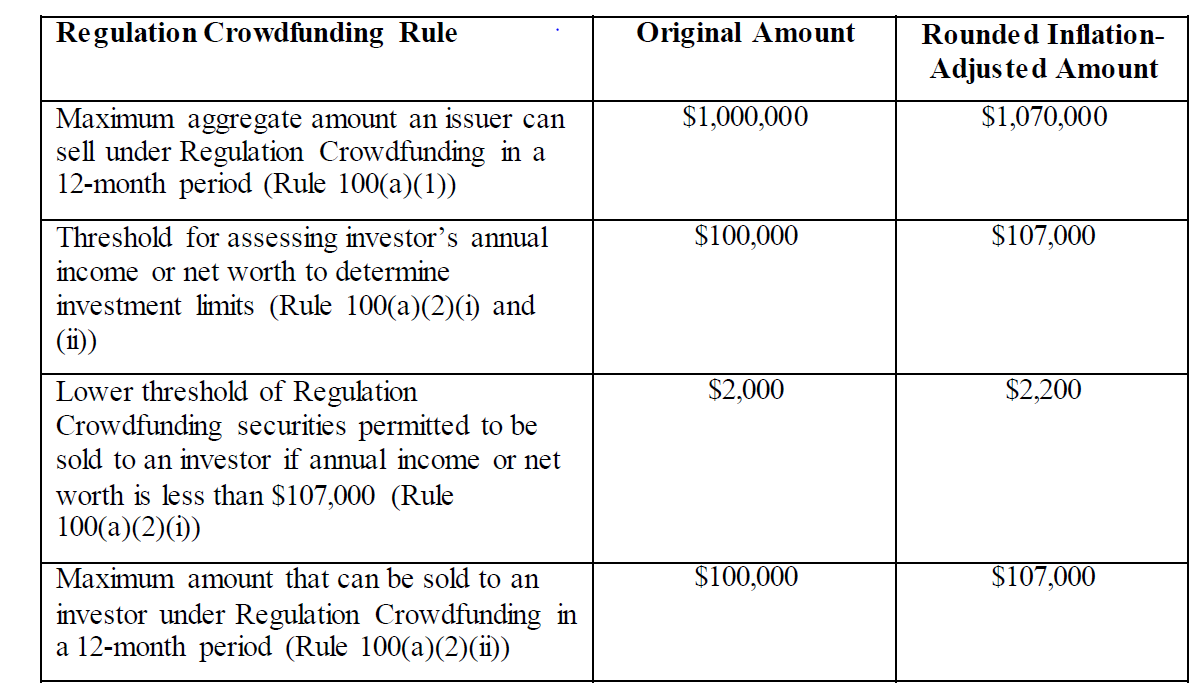

Title III of the JOBS Act, enacted in April 2012, amended the Securities Act to add Section 4(a)(6) to provide an exemption for crowdfunding offerings. Regulation Crowdfunding went into effect on May 16, 2016. For a summary of the provisions, see HERE. The Securities Act requires that the amounts set forth in Regulation Crowdfunding be adjusted by the SEC for inflation not less than once every five years. The SEC is now making its first inflationary increase by amending Rules 100 and 201(t) of Regulation Crowdfunding and Securities Act Form C. The inflation increase is $70,000.

The new offering amount and investment limits are as follows:

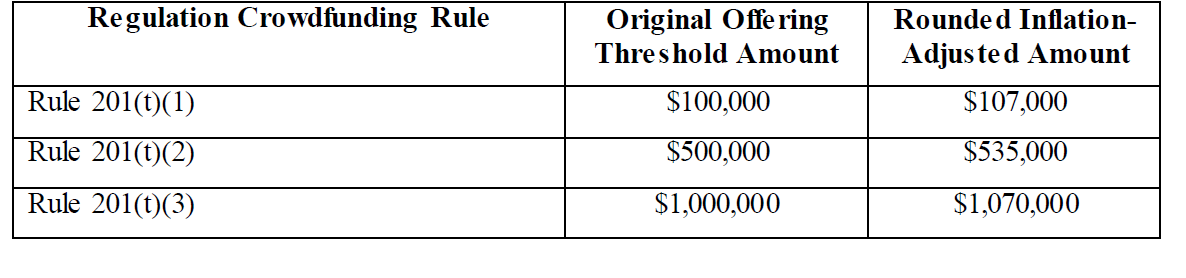

The new financial statement requirement thresholds are as follows:

Technical Amendments to Rules and Forms

Technical Amendments to Rules and Forms

Scaled Disclosure in Registration Forms and Periodic Reports

Section 102(b)(1) of the JOBS Act amended Section 7(a) of the Securities Act to provide that (1) an EGC is permitted to present only two years of audited financial statements in its IPO registration statement, and (2) in any Securities Act registration statement other than its IPO registration statement, an EGC need not present selected financial data under Item 301 of Regulation S-K for any period prior to the earliest audited period presented in its IPO registration statement. However, Item 301 and Rule 3-02 of Regulation S-X and Form 20-F had not been amended for these changes and, until now, contained conflicting requirements. In particular, such rules and forms only addressed reduced disclosure requirements for smaller reporting companies and not address the JOBS Act rules related to EGC’s. The SEC is now amending Item 301 and Rule 3-02 of Regulation S-X and Form 20-F to conform with Section 7(a) of the Securities Act.

Section 102(b)(2) of the JOBS Act amended Section 13(a) of the Exchange Act to provide that an EGC need not present selected financial data in an Exchange Act registration statement or periodic report for any period prior to the earliest audited period presented in the EGC’s first effective registration statement under either the Exchange Act or Securities Act. The SEC is now amending Item 301 of Regulation S-X to conform with Section 13(a) of the Exchange Act.

Likewise, the SEC is amending Item 303 of Regulation S-K related to management discussion and analyses (MD&A) such that a disclosure needs only to be provided for the periods of the financial statements included in the EGC’s IPO registration statement.

Auditor Attestation; Section 404(b) of Sarbanes-Oxley

Section 103 amended Section 404(b) of the Sarbanes-Oxley Act to exempt EGC’s from the need to provide an auditor attestation on management’s assessment of the effectiveness of the EGC’s internal controls over financial reporting. Compliance with Section 404(b) is very expensive, with the average cost being in the $2 million range. To conform with SEC rules and forms to amended Section 404(b), the SEC has amended Article 2-02 of Regulation S-X, Item 308 of Regulation S-K, and Forms 20-F and 40-F to specify that the auditor of an EGC does not need to attest to, and report on, management’s report on internal control over financial reporting and that management does not need to include the auditor’s attestation report in an annual report required by Section 13(a) or 15(d) of the Exchange Act.

Executive Compensation Disclosure and Shareholder Advisory Vote

Section 102(c) of the JOBS Act provides that an EGC need only provide the same executive compensation disclosure as a smaller reporting company. The smaller reporting company executive compensation disclosures are delineated in Items 402(m)-(r) of Regulation S-K. The SEC is amending Item 402 to specify that these scaled disclosures also apply to EGC’s.

Exchange Act Rule 14a-21 requires companies to conduct shareholder advisory votes on say-on-pay, say-on-frequency and golden parachute compensation arrangements with any “named executive officers.” Item 102(a) of the JOBS Act amended Section 14A(e) of the Exchange Act to exempt EGC’s from these requirements. The SEC is amending Exchange Act Rule 14a-21 and Item 402(t) and Instruction 1 to Item 1011(b) of Regulation S-K to conform with this statutory exemption. For more on say-on-pay, say-on-frequency and golden parachute compensation disclosures, see HERE.

Foreign Private Issuers

The definition of an emerging growth company is not dependent on whether the company is domestic or qualifies as a foreign private issuer. A foreign private issuer that qualifies as an EGC may avail itself of the scaled disclosures to the same extent as domestic companies. The SEC is now amending Form 20-F to conform its disclosure requirements with those available to an EGC.

“Check Box” Notice of EGC Status and Compliance with New or Revised Accounting Standards

Section 102(b) of the JOBS Act amended Section 7(a)(2)(B) of the Securities Act and Section 13(a) of the Exchange Act such that an EGC is not required to comply with new or revised financial accounting standards until private companies are also required to comply with those standards. An EGC can, however, choose to comply with such new or revised accounting standards but must do so on the next report or registration statement and notify the SEC of its choice. The election is irrevocable. To provide a method to inform the SEC of its choice, the SEC is adding a “check box” to Securities Act Forms S-1, S-3, S-4, S-8, S-11, F-1, F-3 and F-4 and Exchange Act Forms 10, 8-K, 10-Q, 10–K, 20–F and 40-F.

Click Here To Print- PDF Printout SEC Completes Inflation Adjustment Under Titles I And III Of The Jobs Act; Adopts Technical Amendments

The Author

Laura Anthony, Esq.

Founding Partner

Legal & Compliance, LLC

Corporate, Securities and Going Public Attorneys

330 Clematis Street, Suite 217

West Palm Beach, FL 33401

Phone: 800-341-2684 – 561-514-0936

Fax: 561-514-0832

LAnthony@LegalAndCompliance.com

www.LegalAndCompliance.com

www.LawCast.com

Securities attorney Laura Anthony and her experienced legal team provides ongoing corporate counsel to small and mid-size private companies, OTC and exchange traded issuers as well as private companies going public on the NASDAQ, NYSE MKT or over-the-counter market, such as the OTCQB and OTCQX. For nearly two decades Legal & Compliance, LLC has served clients providing fast, personalized, cutting-edge legal service. The firm’s reputation and relationships provide invaluable resources to clients including introductions to investment bankers, broker dealers, institutional investors and other strategic alliances. The firm’s focus includes, but is not limited to, compliance with the Securities Act of 1933 offer sale and registration requirements, including private placement transactions under Regulation D and Regulation S and PIPE Transactions as well as registration statements on Forms S-1, S-8 and S-4; compliance with the reporting requirements of the Securities Exchange Act of 1934, including registration on Form 10, reporting on Forms 10-Q, 10-K and 8-K, and 14C Information and 14A Proxy Statements; Regulation A/A+ offerings; all forms of going public transactions; mergers and acquisitions including both reverse mergers and forward mergers, ; applications to and compliance with the corporate governance requirements of securities exchanges including NASDAQ and NYSE MKT; crowdfunding; corporate; and general contract and business transactions. Moreover, Ms. Anthony and her firm represents both target and acquiring companies in reverse mergers and forward mergers, including the preparation of transaction documents such as merger agreements, share exchange agreements, stock purchase agreements, asset purchase agreements and reorganization agreements. Ms. Anthony’s legal team prepares the necessary documentation and assists in completing the requirements of federal and state securities laws and SROs such as FINRA and DTC for 15c2-11 applications, corporate name changes, reverse and forward splits and changes of domicile. Ms. Anthony is also the author of SecuritiesLawBlog.com, the OTC Market’s top source for industry news, and the producer and host of LawCast.com, the securities law network. In addition to many other major metropolitan areas, the firm currently represents clients in New York, Las Vegas, Los Angeles, Miami, Boca Raton, West Palm Beach, Atlanta, Phoenix, Scottsdale, Charlotte, Cincinnati, Cleveland, Washington, D.C., Denver, Tampa, Detroit and Dallas.

Contact Legal & Compliance LLC. Technical inquiries are always encouraged.

Follow me on Facebook, LinkedIn, YouTube, Google+, Pinterest and Twitter.

Legal & Compliance, LLC makes this general information available for educational purposes only. The information is general in nature and does not constitute legal advice. Furthermore, the use of this information, and the sending or receipt of this information, does not create or constitute an attorney-client relationship between us. Therefore, your communication with us via this information in any form will not be considered as privileged or confidential.

This information is not intended to be advertising, and Legal & Compliance, LLC does not desire to represent anyone desiring representation based upon viewing this information in a jurisdiction where this information fails to comply with all laws and ethical rules of that jurisdiction. This information may only be reproduced in its entirety (without modification) for the individual reader’s personal and/or educational use and must include this notice.

© Legal & Compliance, LLC 2017

« SEC Adopts The T+2 Trade Settlement Cycle The Senate Banking Committee Passes Several Pro-Business Bills »

SEC Adopts The T+2 Trade Settlement Cycle

Introduction and brief summary of the rule

On March 22, 2017, the SEC adopted a rule amendment shortening the standard settlement cycle for broker-initiated trade settlements from three business days from the trade date (T+3) to two business days (T+2). The change is designed to help enhance efficiency and reduce risks, including credit, market and liquidity risks, associated with unsettled transactions in the marketplace.

Acting SEC Chair Michael Piwowar stated, “[A]s technology improves, new products emerge, and trading volumes grow, it is increasingly obvious that the outdated T+3 settlement cycle is no longer serving the best interests of the American people.” The SEC originally proposed the rule amendment on September 28, 2016. My blog on the proposal can be read HERE. In addition, for more information on the clearance and settlement process for U.S. capital markets, see HERE.

The change amends Rule 15c6-1(a) prohibiting a broker-dealer from effecting or entering into a contract for the purchase or sale of a security that provides for payment of funds and delivery of securities later than T+2, unless otherwise expressly agreed to by the parties at the time of the transaction. This means that when an investor buys a security, the brokerage firm must receive payment from the investor no later than two business days after the trade is executed. Also, when an investor sells a security, the investor must deliver the investor’s security to the brokerage firm no later than two business days after the sale.

The rule does not apply to private exempt transactions such as private placements. The rule also allows a managing underwriter and issuer to agree to a trade settlement cycle other than T+2 as long as the agreement is express and reached at the time of the transaction. Firm commitment offerings are also exempted. In particular, Rule 15c6-1(c) allows registered firm commitment underwritten transactions that price after 4:30 p.m. ET to use a T+3 or T+4 settlement cycle.

The reduction of the settlement cycle to T+2 will also assist in aligning global clearing of securities as many markets, including the United Kingdom and many European countries, are already on the T+2 schedule.

Compliance with the new rules is effective on September 5, 2017.

Background

DTC provides the depository and book entry settlement services for substantially all equity trading in the US. Over $600 billion in transactions are completed at DTC each day. Although all similar, the exact clearance and settlement process depends on the type of security being traded (stock, bond, etc.), the form the security takes (paper or electronic), how the security is owned (registered or beneficial), the market or exchange traded on (OTC Markets, NASDAQ…) and the entities and institutions involved.

All securities trades involve a legally binding contract. In general, the “clearing” of those trades involves implementing the terms of the contract, including ensuring processing to the correct buyer and seller in the correct security and correct amount and at the correct price and date. This process is effectuated electronically.

“Settlement” refers to the fulfillment of the contract through the exchanging of funds and delivery of the securities. In 1993, Exchange Act Rule 15c6-1 was adopted, requiring that settlement occur three business days after the trade date, commonly referred to as “T+3.” Delivery occurs electronically by making an adjusting book entry as to entitlement. One brokerage account is debited and another is credited at the DTC level and a corresponding entry is made at each brokerage firm involved in the transaction. DTC only tracks the securities entitlement of its participating members, while the individual brokerage firms track the holdings in their customer accounts. Technology, of course, plays an important role in the process and ability to efficiently manage settlements.

There may be two brokerage firms between DTC and the customer account holder. Brokerage firms that are direct members with DTC are referred to as “clearing brokers.” Many brokerage firms make arrangements with these DTC members (clearing brokers) to clear the securities on their behalf. Those firms are referred to as “introducing brokers.” A clearing broker will directly route an order through the national exchange or OTC Market, whereas an introducing broker will route the order to a clearing broker, who then routes the order through the exchange or OTC Market.

The Dodd-Frank Act added a definition of, and responsibilities associated with, a “financial market utility” or FMU. Clearing brokers are FMU’s. FMU’s provide the actual functions associated with clearing trades through the DTC system. As part of that process, a division of DTC, the National Securities Clearing Corporation (“NSCC”), becomes the buyer and seller of each contract, netting out and settling all brokerage transactions each day, making one adjusting entry per day. The net entry debits or credits the brokerage firm’s account as necessary. When one of the counterparties in the process does not fulfill its settlement obligations by delivering the securities, there is a “failure to deliver.” Overall, failures to deliver are less than 1% of all transactions.

Likewise, a cash account is maintained for each brokerage firm, which is netted and debited and/or credited each day. These accounts can be in the billions. Clearing firms can either settle each day or carry their open account forward until the next business day. Because all transactions are netted out, 99% of all trade obligations do not require the exchange of money, which helps reduce some risk. NSCC’s role in this process is referred to as a central counterparty or CCP. This process is continuous.

Looking at the process from the top down, the CCP carries the risk that the clearing firm (or FMU) will not have the financial resources to perform its obligations. In turn, the clearing firms have risks from their customers, including introducing brokers, who in turn ultimately have risks from the individual account holders. The risks are compounded by changing values of the securities being traded, during the settlement process. The faster a trade settles, the lower the cumulative risk at each level of the process.

This is a very simplified high-level description of the process. Technically, the roles of DTC and its subsidiaries, CEDE and NSCC, as well as clearing agencies and introducing brokers involve a complex set of regulations, with different definitions, obligations and roles for the different hats the entities wear depending on the type of security being traded (stock, bond, etc.), how the security is owned (registered or beneficial), the form the security takes (paper or electronic), the market or exchange traded on (OTC Markets, NASDAQ…) and the entities and institutions involved (retail or institutional).

Exchange Act Rule 15c6-1

Exchange Act Rule 15c6-1 prohibits a broker-dealer from effecting or entering into a contract for the purchase or sale of a security, subject to certain exemptions, that provides for the payment of the funds or delivery of the securities later than the third business day after the contract (i.e., trade) date unless expressly agreed upon by both parties at the time of the transaction. The rule amendment shortens this time period to two business days.

Exempted securities include government and municipal securities, insurance products, commercial paper, limited partnership units that are not listed on an exchange or automated quotations system (OTC Markets), and sales in a firm commitment underwritten offering that are priced after market close. Firm commitment offerings can rely on an extended T+4 settlement cycle. The new rule does not amend the exemptions or the settlement cycle for firm commitment underwritten offerings.

One of the SEC’s roles is to enhance the resilience and efficiency of the clearance and settlement process such that the system itself does not add to, but rather subtracts from, the risks associated with trading in securities. To further this goal the SEC has amended Rule 15a6-1(a) to shorten the settlement cycle to T+2. The SEC believes this change will reduce various risks in the marketplace, including: (i) the credit risk that one party will be unable to fulfill its delivery obligations (of either cash or the securities) on the settlement date; and (ii) the market risk that the value of the securities will change between the trade and settlement such as to result in a loss to one of the parties.

To drill down further on the summary of the settlement and clearing process described in the background section of this blog, the following is a high-level description of what happens following the execution of a trade. When a trade is submitted to an exchange or alternative trading system (such as OTC Markets), it is matched with a counterparty. That is, a buy order is electronically matched to a sell order. As long as there is a match, the trade is locked in and sent to NSCC.

On the trade date (T), NSCC validates the trade data and communicates receipt of the transaction. At that moment the parties are legally committed to complete the trade. Before the new amendment, at midnight on the first day (T+1), NSCC substitutes itself as the legal buyer and legal seller. Technically, the first buy/sell contract is replaced by two new contracts, one between NSCC and the buyer and the other between NSCC and the seller. The NSCC substitution will now occur at the point of trade comparison and validation.

Historically, on the second day (T+2), NSCC would issue a trade summary report to its members which summarizes all securities and cash to be settled that day, and show the net positions for each. NSCC also sends an electronic instruction to DTC to process the net security and cash settlements. This will now occur on T+1. Finally, on the third day (T+3), DTC process the electronic settlement by transferring cash and securities between the broker-dealer accounts and the broker-dealers, in turn, put the securities and/or cash in their customer accounts. With implementation of the rule change, this final step will be completed on the second day (T+2).

Although institutional trading is similar, there are unique aspects and there can be additional participants. For example, an institution may have a custodian of its securities in addition to its broker, may use a matching provider and may avail itself of different netting and settling processes within the brokerage and DTC systems. Although the detailed process may differ, ultimately both retail and institutional trades will now fully settle in the new T+2 timeline.

As mentioned, the length of the settlement cycle impacts the exposure to credit, market and liquidity risks for the participants. The participants, including NSCC, take measures to reduce these risks, including by requiring funds to be kept on deposit by clearing and brokerage firms effecting such participants’ liquidity. Even then, however, all participants are exposed to market risk during the settlement process, including a decline in value of the traded securities and the risk that such decline could exceed the broker’s capital deposit or result in a failure to deliver.

A reduction in risks would reduce the necessity to mitigate such risk, including reducing the funds that must be kept on deposit by participants. It is undisputed that reducing the settlement cycle reduces these risks. Firms may pass these benefits on to other market participants, including retail investors in the form of reduced margin charges. Also, obviously if funds are tied up for three days pending a settlement of a transaction, whether you are the retail investor or clearing agency, there is a lack of available liquidity to participate in other transactions during that time.

The SEC also believes that shortening the standard settlement cycle will promote technological innovation and changes in market infrastrucutres and operations, incentivizing market participants to make work further to make the markets more efficient.

The rule amendment requires the SEC to conduct a study no later than September 5, 2020, on the impact of the T+2 amendment and the potential impact of further reducing the trade settlement cycle to T+1.

Conforming Stock Exchange Rule Amendments

On February 10, 2017, the SEC approved rulemaking proposals submitted separately by the New York Stock Exchange, the NASDAQ Stock Market and the NYSE MKT that will conform stock exchange rules to the amendments to Rule 15c6-1, with the amendments to become operative concurrently with the SEC compliance date.

Click Here To Print- PDF Printout SEC Adopts The T+2 Trade Settlement Cycle

The Author

Laura Anthony, Esq.

Founding Partner

Legal & Compliance, LLC

Corporate, Securities and Going Public Attorneys

330 Clematis Street, Suite 217

West Palm Beach, FL 33401

Phone: 800-341-2684 – 561-514-0936

Fax: 561-514-0832

LAnthony@LegalAndCompliance.com

www.LegalAndCompliance.com

www.LawCast.com

Securities attorney Laura Anthony and her experienced legal team provides ongoing corporate counsel to small and mid-size private companies, OTC and exchange traded issuers as well as private companies going public on the NASDAQ, NYSE MKT or over-the-counter market, such as the OTCQB and OTCQX. For nearly two decades Legal & Compliance, LLC has served clients providing fast, personalized, cutting-edge legal service. The firm’s reputation and relationships provide invaluable resources to clients including introductions to investment bankers, broker dealers, institutional investors and other strategic alliances. The firm’s focus includes, but is not limited to, compliance with the Securities Act of 1933 offer sale and registration requirements, including private placement transactions under Regulation D and Regulation S and PIPE Transactions as well as registration statements on Forms S-1, S-8 and S-4; compliance with the reporting requirements of the Securities Exchange Act of 1934, including registration on Form 10, reporting on Forms 10-Q, 10-K and 8-K, and 14C Information and 14A Proxy Statements; Regulation A/A+ offerings; all forms of going public transactions; mergers and acquisitions including both reverse mergers and forward mergers, ; applications to and compliance with the corporate governance requirements of securities exchanges including NASDAQ and NYSE MKT; crowdfunding; corporate; and general contract and business transactions. Moreover, Ms. Anthony and her firm represents both target and acquiring companies in reverse mergers and forward mergers, including the preparation of transaction documents such as merger agreements, share exchange agreements, stock purchase agreements, asset purchase agreements and reorganization agreements. Ms. Anthony’s legal team prepares the necessary documentation and assists in completing the requirements of federal and state securities laws and SROs such as FINRA and DTC for 15c2-11 applications, corporate name changes, reverse and forward splits and changes of domicile. Ms. Anthony is also the author of SecuritiesLawBlog.com, the OTC Market’s top source for industry news, and the producer and host of LawCast.com, the securities law network. In addition to many other major metropolitan areas, the firm currently represents clients in New York, Las Vegas, Los Angeles, Miami, Boca Raton, West Palm Beach, Atlanta, Phoenix, Scottsdale, Charlotte, Cincinnati, Cleveland, Washington, D.C., Denver, Tampa, Detroit and Dallas.

Contact Legal & Compliance LLC. Technical inquiries are always encouraged.

Follow me on Facebook, LinkedIn, YouTube, Google+, Pinterest and Twitter.

Legal & Compliance, LLC makes this general information available for educational purposes only. The information is general in nature and does not constitute legal advice. Furthermore, the use of this information, and the sending or receipt of this information, does not create or constitute an attorney-client relationship between us. Therefore, your communication with us via this information in any form will not be considered as privileged or confidential.

This information is not intended to be advertising, and Legal & Compliance, LLC does not desire to represent anyone desiring representation based upon viewing this information in a jurisdiction where this information fails to comply with all laws and ethical rules of that jurisdiction. This information may only be reproduced in its entirety (without modification) for the individual reader’s personal and/or educational use and must include this notice.

© Legal & Compliance, LLC 2017

« SEC Issues Final Rules Requiring Links To Exhibits SEC Completes Inflation Adjustment Under Titles I And III Of The Jobs Act; Adopts Technical Amendments »

SEC Issues Final Rules Requiring Links To Exhibits

On March 1, 2017, the SEC passed a final rule requiring companies to include hyperlinks to exhibits in filings made with the SEC. The amendments require any company filing registration statements or reports with the SEC to include a hyperlink to all exhibits listed on the exhibit list. In addition, because ASCII cannot support hyperlinks, the amendment also requires that all exhibits be filed in HTML format. The rule change was made to make it easier for investors and other market participants to find and access exhibits listed in current reports, but that were originally provided in previous filings.

The SEC first proposed the rule change on August 31, 2016, as discussed in my blog HERE. The new rule continues the SEC’s Division of Corporation Finance’s ongoing Disclosure Effectiveness Initiative. I anticipate that this initiative will not only continue but gain traction in the coming years under the new administration as, hopefully, more duplicative, antiquated and immaterial requirements come under scrutiny. At the end of this blog, I include an up-to-date summary of the proposals and request for comment related to the ongoing Disclosure Effectiveness Initiative.

Background

On April 15, 2016, the SEC issued a 341-page concept release and request for public comment on sweeping changes to certain business and financial disclosure requirements in Regulation S-K (“S-K Concept Release”). The S-K Concept Release contained a discussion and request for comment on exhibit filing requirements. Item 601 of Regulation S-K specifies the exhibits that must be filed with registration statements and SEC reports. Item 601 requires the filing of certain material contracts, corporate documents, and other information as exhibits to registration statements and reports.

A particular area of discussion recently has been the need to file schedules to contracts. These schedules can be lengthy and lack materiality. Likewise, a recent area of discussion has been the necessity of filing an immaterial amendment to a material exhibit. The S-K Concept Release contains a lengthy discussion on exhibits, including drilling down on specific filing requirements. Many of the exhibit filing requirements are principle-based, including, for example, quantitative thresholds for contracts. Consistent with the rest of the S-K Concept Release, the SEC discusses whether these standards should be changed to a straight materiality approach. The SEC also discusses eliminating some exhibit filing requirements altogether, such as where the information is otherwise fleshed out in financial statements or other disclosures (for example, a list of subsidiaries).

Currently companies are allowed to reference exhibits filed in prior filings as opposed to refiling the exhibit with the SEC. The better practice has always been to include a specific reference to the filing, including the date of the filing, and where the original exhibit can be located. However, many companies do not do so, leaving the public to search through prior filings to find the listed exhibit. Moreover, as time goes by and companies switch counsel, some choose not to spend the time and funds to have new counsel update an exhibit list to include a full reference. The new rule will require them to do so. The rule amendment is limited to the presentation of the exhibit list and requires including a hyperlink to the actual filed exhibit.

Rule Amendments

In addition to the filing of exhibits and schedules, Item 601 of Regulation S-K requires each company to include an exhibit index list that lists each exhibit included as part of the filing. The list is cumulative. For example, the company’s articles of incorporation are required to be included as an exhibit with every 10-Q and 10-K filing. Once an exhibit has been filed once, the company could historically incorporate by reference by including a footnote as to which filing the original exhibit can be found in. Unfortunately, I find that companies often will indicate that an exhibit has been previously filed, without giving a specific reference as to which filing or when, leaving an investor or reviewer to go fish. The SEC rightfully asserts that requiring companies to include hyperlinks from the exhibit index to the actual exhibits filed would allow much easier access to these filings.

The new rule change would requires companies to include a hyperlink to each filed exhibit on the exhibit index as required by Item 601 of Regulation S-K, for virtually all filings made with the SEC, including XBRL exhibits. An active hyperlink will now be required in all filings made under the Securities Act or Exchange Act, provided however that if the filing is a registration statement, the active hyperlinks need only be included in the version that becomes effective.

Currently exhibits may be filed in the EDGAR system in either ASCII or HTML format. HTML format allows for hyperlinks to another place within the same document or to a separate document. ASCII does not support such hyperlinks. Over the years HTML has become the standard used for EDGAR filings, with 99% of filings in 2015 using HTML. The rule amendment will now prohibit the use of ASCII for exhibits and require only HTML with the newly required hyperlinks.

In addition, the rule changes include conforming changes to Rule 105 of Regulation S-T. Rule 105 sets forth the limitations and liabilities for the use of hyperlinks. Rule 105 allows hyperlinks to other documents within the same filing or previously filed documents on EDGAR but prohibits hyperlinks to sites, locations, or documents outside the EDGAR system.

The new Rule goes into effect on September 1, 2017, provided however that non-accelerated filers and smaller reporting companies that submit filings in ASCII may delay compliance through September 1, 2018.

Further Background

I have been keeping an ongoing summary of the SEC’s ongoing Disclosure Effectiveness Initiative. The following is a recap of such initiative and proposed and actual changes. However, I note that with the recent election, and the GOP sweeping control of both the House and Senate, it is unclear what the future of these initiatives holds.

On August 31, 2016, the SEC issued proposed amendments to Item 601 of Regulation S-K to require hyperlinks to exhibits in filings made with the SEC. The proposed amendments would require any company filing registration statements or reports with the SEC to include a hyperlink to all exhibits listed on the exhibit list. In addition, because ASCII cannot support hyperlinks, the proposed amendment would also require that all exhibits be filed in HTML format. See my blog HERE on the Item 601 proposed changes.

On August 25, 2016, the SEC requested public comment on possible changes to the disclosure requirements in Subpart 400 of Regulation S-K. Subpart 400 encompasses disclosures related to management, certain security holders and corporate governance. See my blog on the request for comment HERE.

On July 13, 2016, the SEC issued a proposed rule change on Regulation S-K and Regulation S-X to amend disclosures that are redundant, duplicative, overlapping, outdated or superseded (S-K and S-X Amendments). See my blog on the proposed rule change HERE.

That proposed rule change and request for comments followed the concept release and request for public comment on sweeping changes to certain business and financial disclosure requirements issued on April 15, 2016. See my two-part blog on the S-K Concept Release HERE and HERE.

As part of the same initiative, on June 27, 2016, the SEC issued proposed amendments to the definition of “Small Reporting Company” (see my blog HERE). The SEC also previously issued a release related to disclosure requirements for entities other than the reporting company itself, including subsidiaries, acquired businesses, issuers of guaranteed securities and affiliates. See my blog HERE.

As part of the ongoing Disclosure Effectiveness Initiative, in September 2015 the SEC Advisory Committee on Small and Emerging Companies met and finalized its recommendation to the SEC regarding changes to the disclosure requirements for smaller publicly traded companies. For more information on that topic and for a discussion of the reporting requirements in general, see my blog HERE.

In March 2015 the American Bar Association submitted its second comment letter to the SEC making recommendations for changes to Regulation S-K. For more information on that topic, see my blog HERE.

In early December 2015 the FAST Act was passed into law. The FAST Act requires the SEC to adopt or amend rules to: (i) allow issuers to include a summary page to Form 10-K; and (ii) scale or eliminate duplicative, antiquated or unnecessary requirements for emerging-growth companies, accelerated filers, smaller reporting companies and other smaller issuers in Regulation S-K. The current Regulation S-K and S-X Amendments are part of this initiative. In addition, the SEC is required to conduct a study within one year on all Regulation S-K disclosure requirements to determine how best to amend and modernize the rules to reduce costs and burdens while still providing all material information. See my blog HERE.

Click Here To Print- PDF Printout SEC Issues Final Rules Requiring Links To Exhibits

The Author

Laura Anthony, Esq.

Founding Partner

Legal & Compliance, LLC

Corporate, Securities and Going Public Attorneys

330 Clematis Street, Suite 217

West Palm Beach, FL 33401

Phone: 800-341-2684 – 561-514-0936

Fax: 561-514-0832

LAnthony@LegalAndCompliance.com

www.LegalAndCompliance.com

www.LawCast.com

Securities attorney Laura Anthony and her experienced legal team provides ongoing corporate counsel to small and mid-size private companies, OTC and exchange traded issuers as well as private companies going public on the NASDAQ, NYSE MKT or over-the-counter market, such as the OTCQB and OTCQX. For nearly two decades Legal & Compliance, LLC has served clients providing fast, personalized, cutting-edge legal service. The firm’s reputation and relationships provide invaluable resources to clients including introductions to investment bankers, broker dealers, institutional investors and other strategic alliances. The firm’s focus includes, but is not limited to, compliance with the Securities Act of 1933 offer sale and registration requirements, including private placement transactions under Regulation D and Regulation S and PIPE Transactions as well as registration statements on Forms S-1, S-8 and S-4; compliance with the reporting requirements of the Securities Exchange Act of 1934, including registration on Form 10, reporting on Forms 10-Q, 10-K and 8-K, and 14C Information and 14A Proxy Statements; Regulation A/A+ offerings; all forms of going public transactions; mergers and acquisitions including both reverse mergers and forward mergers, ; applications to and compliance with the corporate governance requirements of securities exchanges including NASDAQ and NYSE MKT; crowdfunding; corporate; and general contract and business transactions. Moreover, Ms. Anthony and her firm represents both target and acquiring companies in reverse mergers and forward mergers, including the preparation of transaction documents such as merger agreements, share exchange agreements, stock purchase agreements, asset purchase agreements and reorganization agreements. Ms. Anthony’s legal team prepares the necessary documentation and assists in completing the requirements of federal and state securities laws and SROs such as FINRA and DTC for 15c2-11 applications, corporate name changes, reverse and forward splits and changes of domicile. Ms. Anthony is also the author of SecuritiesLawBlog.com, the OTC Market’s top source for industry news, and the producer and host of LawCast.com, the securities law network. In addition to many other major metropolitan areas, the firm currently represents clients in New York, Las Vegas, Los Angeles, Miami, Boca Raton, West Palm Beach, Atlanta, Phoenix, Scottsdale, Charlotte, Cincinnati, Cleveland, Washington, D.C., Denver, Tampa, Detroit and Dallas.

Contact Legal & Compliance LLC. Technical inquiries are always encouraged.

Follow me on Facebook, LinkedIn, YouTube, Google+, Pinterest and Twitter.

Legal & Compliance, LLC makes this general information available for educational purposes only. The information is general in nature and does not constitute legal advice. Furthermore, the use of this information, and the sending or receipt of this information, does not create or constitute an attorney-client relationship between us. Therefore, your communication with us via this information in any form will not be considered as privileged or confidential.

This information is not intended to be advertising, and Legal & Compliance, LLC does not desire to represent anyone desiring representation based upon viewing this information in a jurisdiction where this information fails to comply with all laws and ethical rules of that jurisdiction. This information may only be reproduced in its entirety (without modification) for the individual reader’s personal and/or educational use and must include this notice.

© Legal & Compliance, LLC 2017

« The Acting SEC Chair Has Trimmed Enforcement’s Subpoena Power SEC Adopts The T+2 Trade Settlement Cycle »

The Acting SEC Chair Has Trimmed Enforcement’s Subpoena Power

In early February 2017, acting SEC Chair Michael Piwowar revoked the subpoena authority from approximately 20 senior SEC enforcement staff. The change leaves the Director of the Division of Enforcement as the sole person with the authority to approve a formal order of investigation and issue subpoenas. Historically, the staff did not have subpoena power; however, in 2009 then Chair Mary Shapiro granted the staff the power, in the wake of the Bernie Madoff scandal. Chair Shapiro deemed the policy to relate solely to internal SEC procedures and, as such, passed the delegation of power without formal notice or opportunity for public comment.

This is the beginning of what I expect will be many, many changes within the SEC as the new administration changes the focus of the agency from Mary Jo White’s broken windows policies to supporting capital formation. The mission of the SEC is to protect investors, maintain fair, orderly and efficient markets and facilitate capital formation. Although each mission should be a priority, the reality is that the focus of the SEC changes based on its Chair and Commissioners and political pressure. Mary Jo White viewed the SEC enforcement division and the task of investor protection as her top priority. Mike Piwowar and presumably Jay Clayton are shifting the top priority to capital formation.

Acting Chair Piwowar has been a vocal critic of both the staff subpoena power and the manner in which the power was created since its inception. He has also been a vocal critic of the SEC’s investigative power, believing it has too much power and too little oversight.

Mr. Piwowar made a speech in 2013 to the LA County Bar, being very clear about his views on the SEC and its operations. At the time, he talked about enforcement and that investigations should be focused on evidence of wrongdoing, to wit: lying, cheating and stealing. He stated that the SEC must only concern itself with “the facts known to them and the reasonable inferences from those facts” and cautioning that a Commissioner “should never suggest, vote for, or participate in an investigation aimed at a particular individual for reasons of animus, prejudice, or vindictiveness.” In that regard, he recognizes that “the mere existence of an investigation – even without taking any subsequent enforcement action – carries with it the power to defame and destroy.”

Piwowar then went on to specifically address the process for the issuance of a formal order of investigation, which brings with it the power to subpoena witnesses, documents and testimony. He stated, “Historically, formal orders have been approved by the Commission. This process usually required the staff to prepare a memorandum for the Commission containing a summary of the case and any possible violations, and recommending issuance of the order. Although it was rare, if ever, for the Commission to deny a request for a formal order, the process brought forth a certain level of focus and review from not only the Division of Enforcement, but also staff in the Office of the General Counsel as well as the other divisions, such as Corporation Finance, Trading and Markets, and Investment Management.” Piwowar continued, “[B]ut in a significant departure from past practice, in August 2009, the Commission delegated the authority to issue formal orders to the Director of Enforcement, on the grounds that such delegation would expedite the investigative process by reducing the time and paperwork previously associated with obtaining Commission authorization prior to issuing subpoenas.”

Moreover, clearly this change made formal orders much easier to obtain, as evidenced by the fact that the issuance of these orders doubled in the years following. Mr. Piwowar stated, “[t]he delegation of authority for approval of formal orders was deemed by the Commission to relate solely to agency organization, procedure, and practice, and therefore not subject to the notice and comment process under the Administrative Procedure Act. The mere fact that we can institute certain rules without obtaining comment from the public does not necessarily mean that we should. Given the significant ramifications for persons who are on the receiving end of a subpoena issued pursuant to a formal order, we should make sure that public comment is allowed on any review of the formal order process.”

It is no surprise, then, that Piwowar remanded this provision as soon as he was in a position to do so.

Potential Additional Changes with Enforcement and SEC Policy

Incoming SEC Chair Jay Clayton is largely thought to be pro-business and likely sympathetic to large financial institutions. Moreover, the SEC still must appoint additional Commissioners and a new Director of Enforcement. The individuals that fill these roles will undoubtedly greatly influence policy.

Mr. Clayton has made public comments criticizing the Dodd-Frank Act for over-regulating the financial services industry. As such, I would expect to see changes in Dodd-Frank and a lack of interest in enforcing some provisions while they remain.

Clayton has also publicly criticized the Foreign Corrupt Practices Act (FCPA) as putting U.S. businesses at a huge disadvantage against competitors not subject to this law, such as those domiciled in other countries. Clayton specifically stated that U.S. companies were disproportionately affected by a “virtually stand-alone approach to deterring foreign corruption” that “places significant costs on companies subject to the FCPA as compared to their competitors that are not.” Trump also spoke against the FCPA. Accordingly, it is very likely that enforcement of FCPA violations will take a low priority going forward.

Another area in which Clayton will not likely focus is enforcement of whistleblower retaliation cases. Over the past few years the SEC has vigorously pursued enforcement proceedings against companies thought to retaliate against or even chill whistleblower activity. The SEC has even taken action against contract provisions in employment or severance agreements that could be deemed to prevent or impede whistleblower activity. For more on this topic, see my blog HERE. Likewise, the Financial Choice Act 2.0 contains provisions reducing the availability of whistleblower awards.

On February 3, 2017, President Trump signed an executive order entitled “Core Principles for Regulating the United States Financial System.” The order set forth seven principles for regulating the financial system, including:

(a) empower Americans to make independent financial decisions and informed choices in the marketplace, save for retirement, and build individual wealth;

(b) prevent taxpayer-funded bailouts;

(c) foster economic growth and vibrant financial markets through more rigorous regulatory impact analysis that addresses systemic risk and market failures, such as moral hazard and information asymmetry;

(d) enable American companies to be competitive with foreign firms in domestic and foreign markets;

(e) advance American interests in international financial regulatory negotiations and meetings;

(f) make regulation efficient, effective and appropriately tailored; and

(g) restore public accountability within federal financial regulatory agencies and rationalize the federal financial regulatory framework.

The executive order, although general, certainly is very telling in regard to the philosophy of this administration, including that which is related to over-regulation and enforcement by the SEC.

Administrative Proceedings

The SEC Penalties Act, as written in its beginning form, treats administrative court and federal court proceedings equally. However, the administrative court process is not an equal forum and, based on a barrage of negative attacks, including lawsuits, appeals and media coverage, requires review and attention. An analysis by The Wall Street Journal in 2015 indicated that in the last five years, the SEC has won 90% of cases brought in its own administrative courts but only 69% of cases brought in federal court. Part of the disparity could be that the SEC chooses to settle or drop “losing” claims, but that still leaves a large discrepancy.

Moreover, the Dodd-Frank Act, enacted in 2010, for the first time granted the SEC the authority to impose civil penalties in administrative proceedings against any person the SEC claims violated the securities laws, regardless of whether that person or firm is in the securities business. In other words, Dodd-Frank opened the doors for the SEC’s own administrative proceedings to be just another forum for the pursuit of any securities law violations. Common sense tells us that this change, seven years ago, directly relates to the uproar in the defensive bar.

Over the past years a slew of cases have been filed challenging the SEC’s power in administrative actions and the administrative process. With little fanfare or public announcement, the SEC under Jay Clayton may cut back dramatically on the use of administrative proceedings, quietly ending or at least greatly reducing this battle until more formal policy changes are brought.

Click Here To Print- PDF Printout The Acting SEC Chair Has Trimmed Enforcement’s Subpoena Power

The Author

Laura Anthony, Esq.

Founding Partner

Legal & Compliance, LLC

Corporate, Securities and Going Public Attorneys

330 Clematis Street, Suite 217

West Palm Beach, FL 33401

Phone: 800-341-2684 – 561-514-0936

Fax: 561-514-0832

LAnthony@LegalAndCompliance.com

www.LegalAndCompliance.com

www.LawCast.com

Securities attorney Laura Anthony and her experienced legal team provides ongoing corporate counsel to small and mid-size private companies, OTC and exchange traded issuers as well as private companies going public on the NASDAQ, NYSE MKT or over-the-counter market, such as the OTCQB and OTCQX. For nearly two decades Legal & Compliance, LLC has served clients providing fast, personalized, cutting-edge legal service. The firm’s reputation and relationships provide invaluable resources to clients including introductions to investment bankers, broker dealers, institutional investors and other strategic alliances. The firm’s focus includes, but is not limited to, compliance with the Securities Act of 1933 offer sale and registration requirements, including private placement transactions under Regulation D and Regulation S and PIPE Transactions as well as registration statements on Forms S-1, S-8 and S-4; compliance with the reporting requirements of the Securities Exchange Act of 1934, including registration on Form 10, reporting on Forms 10-Q, 10-K and 8-K, and 14C Information and 14A Proxy Statements; Regulation A/A+ offerings; all forms of going public transactions; mergers and acquisitions including both reverse mergers and forward mergers, ; applications to and compliance with the corporate governance requirements of securities exchanges including NASDAQ and NYSE MKT; crowdfunding; corporate; and general contract and business transactions. Moreover, Ms. Anthony and her firm represents both target and acquiring companies in reverse mergers and forward mergers, including the preparation of transaction documents such as merger agreements, share exchange agreements, stock purchase agreements, asset purchase agreements and reorganization agreements. Ms. Anthony’s legal team prepares the necessary documentation and assists in completing the requirements of federal and state securities laws and SROs such as FINRA and DTC for 15c2-11 applications, corporate name changes, reverse and forward splits and changes of domicile. Ms. Anthony is also the author of SecuritiesLawBlog.com, the OTC Market’s top source for industry news, and the producer and host of LawCast.com, the securities law network. In addition to many other major metropolitan areas, the firm currently represents clients in New York, Las Vegas, Los Angeles, Miami, Boca Raton, West Palm Beach, Atlanta, Phoenix, Scottsdale, Charlotte, Cincinnati, Cleveland, Washington, D.C., Denver, Tampa, Detroit and Dallas.

Contact Legal & Compliance LLC. Technical inquiries are always encouraged.

Follow me on Facebook, LinkedIn, YouTube, Google+, Pinterest and Twitter.

Legal & Compliance, LLC makes this general information available for educational purposes only. The information is general in nature and does not constitute legal advice. Furthermore, the use of this information, and the sending or receipt of this information, does not create or constitute an attorney-client relationship between us. Therefore, your communication with us via this information in any form will not be considered as privileged or confidential.

This information is not intended to be advertising, and Legal & Compliance, LLC does not desire to represent anyone desiring representation based upon viewing this information in a jurisdiction where this information fails to comply with all laws and ethical rules of that jurisdiction. This information may only be reproduced in its entirety (without modification) for the individual reader’s personal and/or educational use and must include this notice.

© Legal & Compliance, LLC 2017

« The Financial Choice Act 2.0 SEC Issues Final Rules Requiring Links To Exhibits »